Deprecated: Creation of dynamic property FusionSC_Column::$is_nested is deprecated in /home/wpfsi1/public_html/wp-content/plugins/fusion-builder/inc/class-fusion-column-element.php on line 511

Today, if you own a business or are thinking about starting a business, or a consumer, good credit is critical in making sound financial decisions and not an option. Unfortunately, many small business owners (and consumers) have poor credit which always haunts them as they try to build and establish their businesses.

Not knowing how credit works, how your credit score is calculated, how to improve your credit score and maintain it, how to contest errors on your credit report and how to read your credit report correctly are the primary reasons small business owners fail to get the necessary capital needed to successfully grow their businesses.

Why Business Credit Is Important!

Importance of Establishing Business Credit

We have provided the excerpt below by Scott Letourneau which provided additional information on the importance of establishing and maintaining good business credit.

Think of companies like Google, Facebook, and Apple. Did they rely only on their own money for growth? No. Even if you have strong sales and plenty of cash in the bank now, a day will come when you’ll need additional cash support to overcome an unexpected twist in your business. It might be the loss of a key vendor, partner, employee or client, but the companies that beat the odds are the ones who are in a position to access OPM to bridge those tough times when they come. They don’t have to rely on their own cash reserves because they followed a clear plan from day one to build good business credit.

Most business owners learn the hard way that the day you need credit is not the time to start building it.

George Ross, the attorney for Donald Trump said, “The time to go to the banks is BEFORE you need the money.” Similarly, the time to start building business credit is the moment you form your business entity. That is when the business credit bureaus will start developing a file on your business. They say that the best day to plant a tree is ten years ago, and the second best day is today! If you missed that ideal starting point, the time is NOW to build your company’s business credit profile so you’re in a position to help your business grow.

These aren’t just opinions. The biggest authorities in the credit world agree that this subject is critically important to small business owners. What do they have to say?

![]()

The Small Business Administration (SBA) is clear on the importance of a business credit report. “If you are already in business, you should be prepared to submit a credit report for your business. As with the personal credit report, it is important to review your business’ credit report before beginning the [SBA] application process.”

According to Dun & Bradstreet, managing risk is critical to the success of every business. That’s why banks, vendors, suppliers, and partners turn to D&B data to check a company’s creditworthiness before they’ll enter into any contractual arrangement. They advise every lender to check the ability of a business to pay on time before setting credit terms.

The Equifax reporting bureau issues similar warnings. “Understand your Business Relationships! Before you sign a contract with a key partner/supplier or ship that big customer order, make sure you know who you’re doing business with.”

According to Corporate Experian, creditors and suppliers are increasingly using business reports to make lending and credit decisions. That’s why it’s important to establish a separate credit report for your business. If your business is new, or if you haven’t yet established business credit, obtaining trade-lines (vendor lines of credit) is a great way to begin building your business credit report.

They go on to say that, “A small business score is vital for separating your personal and business financial risk. As a forward-thinking small business owner, you know that credit affects your ability to obtain capital to develop your small business.” Your business credit report can influence:

- The amount of your loan and what interest rates you’ll pay

- The cost of your business insurance premiums

- The credit terms your suppliers will extend to your company

Entrepreneur Magazine stresses the importance of keeping business credit reports separate from your personal credit. “Fewer than 10% of all entrepreneurs know about or truly understand how business credit is established and tracked and how it affects their lives and businesses.

Conventional wisdom has been that there are no consequences to using personal credit cards, home equity line or a personal guarantee for a business. While it can make getting started easier, your personal assets may be at risk if vendors pay late, contracts are put on hold or orders are canceled.”

That’s a sample what the big sources of business credit information have to say on the subject. So, what about the sources of the money? Here’s what the big banks say about the importance of business credit and how they lend money to business owners:

Both Citi and Wells Fargo are on record as saying that business and personal credit are both important factors when they’re making decisions on business loans and lines of credit.

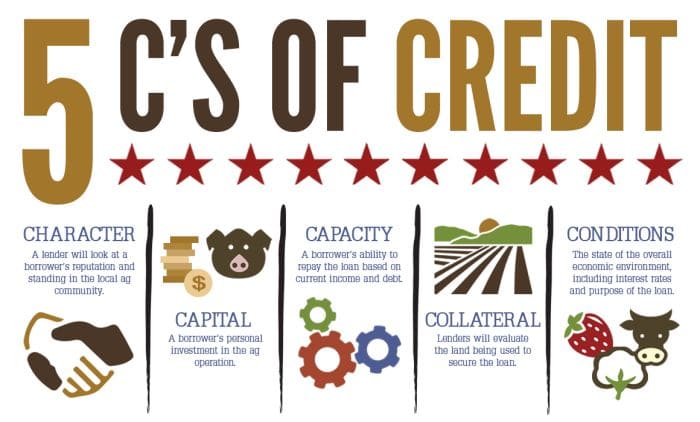

Wells Fargo uses the “Five Cs” of business credit approval when considering credit.

So, now that we have some background on the importance of solid business credit, let’s get specific on how it works and how to establish it. There are three critical questions that all new business owners must consider, even before their first day of operation:

1. How long does it take to properly build business credit?

Business credit is a generic term, but there are two main types – cash lines of credit, and vendor lines of credit (also known as trade-lines). When we talk about business credit, most people think of bank lines of credit that are immediately available as cash. Most new companies can’t qualify for these until they build up trade-lines with vendors who will report their payment history to the business credit bureaus. It can take 2-4 years to build strong business credit profiles with the big three, Dun & Bradstreet, Corporate Experian, and Corporate Equifax.

That’s if you do it right and if you work with any vendors that report to these bureaus. There are over 50,000 vendors that grant business lines of credit, yet less than 10% of them report to the bureaus. For this reason, odds are that even if you’re paying all your vendors on time, your scores are low or nonexistent. Establishing trade-lines with vendors is not the only way to quickly start building up a business credit profile, but it’s one of the most important ones. That history becomes critical when you to apply cash lines of credit with banks, merchant account cash advances or SBA loans.

2. What are the consequences if I make a mistake?

This is not like your personal credit score where if something is inaccurate you can submit a letter to either Transunion, Equifax, or Experian and they are required by law to reply and to abide by certain standards of fairness and responsiveness.

The business credit bureaus don’t have any such rules. The system is far less forgiving and a lot more difficult to navigate. There’s no oversight on how they operate or when and how they update your file based on the EIN number of your entity. You really have just one shot at building your profile properly from the start. Any mistake, as small as being one digit off on an address (or worse yet, being out of compliance) can “red flag” your business and YOUR NAME as high risk for this and any other businesses you form in the future!

3. Is this something I can put off until later?

As you can already tell from the previous two questions, waiting until later is extremely risky. Building business credit is a process that requires a system to do it fast and accurately! Following a proper sequence to get the best results in the shortest period of time to is what sets Fast Business Credit apart. The other factor is honesty. When you work with Fast Business Credit, we let you know up front how much credit your business can secure, what types are available to you and how long it will take.

No matter what you may have heard, there’s no “cookie cutter” approach out there. Results will vary just as they do in personal finance. This will depend on several factors, including but not limited to the length of time in business, gross revenues, net profits, merchant account revenue, your personal credit, how many vendors are currently reporting and much more.

Don’t wait! Here are the up-front steps to take to ensure that creditors and suppliers can validate your business information:

- Incorporate or form an LLC (Limited Liability Company) to ensure that your company is seen as a separate business entity

- Obtain a federal Employer Identification Number (EIN)

- Open business bank accounts in your legal business name

- Set up a dedicated business phone line in your business name and make sure it’s listed

Being successful in today’s ever-changing economic environment requires that your business is both credible and fundable and that requires a system to build business credit fast (and with accuracy)!

You will learn at our Credit Workshop:

- How credit works

- How your credit score is calculated

- How to improve your score fast and maintain it

- How to contest errors

- How to read your credit report

Creditable sources:

http://www.experian.com/small-business/small-business-credit.jsp

http://www.sba.gov/content/business-loan-application-checklist

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment