Why the Racial Wealth Gap Won’t Go Away

Wealth Inequality

Wealth inequality can be described as the unequal distribution of assets within a population. The United States exhibits wider disparities of wealth between rich and poor than any other major developed nation. Definition provided by Inequality.org

Defining Wealth

Wealth is equated with “net worth,” the sum total of your assets minus liabilities. Assets can include everything from an owned personal residence and cash in savings accounts to investments in stocks and bonds, real estate, and retirement accounts. Liabilities, on the other hand, are what a household owes out: a car loan, credit card balance, student loan, mortgage, or any other bill yet to be paid.

In the United States, wealth inequality runs even more pronounced than income inequality.

The Racial Wealth Divide

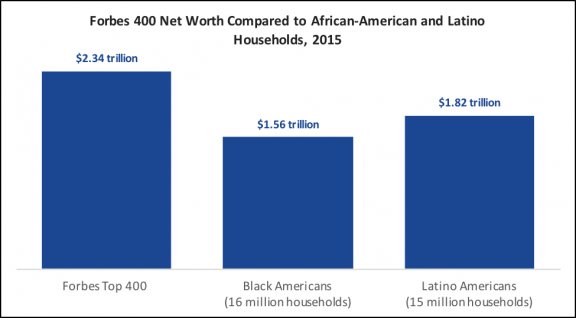

The billionaires who make up the Forbes 400 list of richest Americans now have as much wealth as all African-American households, plus one-third of America’s Latino population, combined. In other words, just 400 extremely wealthy individuals have as much wealth as 16 million African-American households and 5 million Latino households.

Read: Why the racial wealth gap won’t go away

The Roots of the Widening Racial Wealth Gap

According to a 2009 study by Brandeis University’s Institute on Assets and Social Policy home ownership is the single largest factor in driving racial wealth inequality.

The study followed 1,700 families for 25 years, starting in 1984. During that time, “the total wealth gap between white and African-American families nearly triples, increasing from $85,000 in 1984 to $236,500 in 2009.” (This is insane.) The contributing factors to this wealth gap were as follows:

Among households with positive wealth growth during the 25-year study period, the number of years of home ownership accounts for 27 percent of the difference in relative wealth growth between white and African-American families, the largest portion of the growing wealth gap. The second largest share of the increase, accounting for 20 percent, is average family income. Highly educated households correlate strongly with larger wealth portfolios, but similar college degrees produce more wealth for whites, contributing 5 percent of the proportional increase in the racial wealth gap. Inheritance and financial support from family combine for another 5 percent of the increasing gap. How much wealth a family started out with in 1984 also predicts a portion (3 percent) of family wealth 25 years later.

Black people tend to buy houses later in life; therefore, their houses do not increase in value as much. They also tend to live in black neighborhoods, where real estate values are lower since white people don’t want to buy there. Black people also inherit far less money, and they are not able to build wealth through marriage as easily as white people. This much, by itself, adds up to a self-perpetuating system in which whites steadily increase their own wealth, while black families mostly cannot.

Add in poorer education, and fewer employment opportunities, and institutional racism, and you have a very, very steep hole for black families collectively to climb out of. And it will take a very, very massive public investment to change it.

What Is the Solution To The Wealth Gap Problem?

Experts of Color Network (ECON), which includes over 200 of the nation’s leading Native American, Asian-American, African-American, Latino, and Native Hawaiian experts on housing, jobs, savings and investment to debt, credit, social insurance, and business development recommends that policymakers consider the following principles when developing policies, in order to create inclusive economic participation:

- Policies must be designed to change the structures of economic opportunity.

- Policies must help people build assets throughout their lifetime.

- Policies must help communities build and retain wealth.

- Policies must be both universal and targeted to America’s more vulnerable communities.

As with many “think tank” and academic solutions, most of these are rooted in “policy changes”. The inherent problem with this mode of thinking is that the poor and disenfranchised are left waiting for politicians to make changes in a system that is ultimately controlled by the wealthy.

The idea of policy change has been argued for the last 50 years.While the rhetoric has changed, the core argument has remained the same.

In addition to any governmental policy change, there must be a paradigm shift in the affected communities with regard to saving and spending habits. We need the think about solutions in a new way.

For a fresh perspective and actionable steps you can take to address the wealth gap you’re invited to join the conversation, There’s Money Out There on July 16th at 1:00 pm on WURD 900 AM.

Creative approaches to personal wealth will be discussed with guests Pamela Jolly and Reggie Kyle; financial experts who have crafted alternative solutions for African Americans to address the Wealth Gap problem. You will want to tune in for what promises to be a vibrant and revealing conversation with practical advice that you can implement right away.

To learn more about the TMOT show, click here.

Why the Racial Wealth Gap Won't Go Away Wealth Inequality Wealth inequality can be described as the unequal distribution of assets within a population. The United States exhibits wider disparities of wealth between rich and poor than any other major developed nation. Definition provided by Inequality.org Defining Wealth Wealth is equated with “net worth,” [...]

The post Wealth Inequality: The Racial Wealth Gap appeared first on WPFSI.

]]>The post Wealth Inequality: The Racial Wealth Gap appeared first on WPFSI.

Recently while working on a loan request for submission to our Loan Committee, I thought about the inherent risks involved in staring and growing a business. “There is an old saying that good lawyers run away from risk, while good businessmen run towards risk”. Risks, in and of itself, can be a good thing if [...]

The post New Business Risks: 5 risks to consider when launching a business appeared first on WPFSI.

]]>Notice: ob_end_clean(): Failed to delete buffer. No buffer to delete in /home/wpfsi1/public_html/wp-content/plugins/wp-optin-boxes-pro/public/class.public.php on line 654

The challenge is to avoid the bad risks, while actively seeking and managing the smart risks. There are no guarantees in business, but it pays to learn from the experiences of entrepreneurs and business experts who have gone before you. Below are a few of the risks that the typical lender/investor look for in new startups:

1. Product risk-Decide what you are selling;

2. Market risk-Knowing your customer and why, how and where they buy related products is a very important risk factor to assess before launching your product;

3. Financial risk- Make sure to identify key business milestones and schedules that clearly identify the points in time when equity or debt investments are necessary to reach the next growth level;

4. Team risk-Make sure that you have a great team to help you continue to assess risk and help develop and implement business strategies

For additional information about loans, lending or small business planning, especially in Philadelphia, please call Calvin R. Tucker at 215-452-0100 or email me at calvin@wpfsi.com. Visit WPFSI’s website at www.wpfsi.com.

“Your neighborhood’s business leader”

The post New Business Risks: 5 risks to consider when launching a business appeared first on WPFSI.

]]>As the New Year is upon us, it is time for all business owners to take stock of the health of their respective companies. Let’s look at the historical performance of the business as a gateway to predict future performance of the business. According to the “Business Ferret” (a monthly financial analysis for Business Owners), [...]

The post Reviewing Your Business Performance appeared first on WPFSI.

]]>Notice: ob_end_clean(): Failed to delete buffer. No buffer to delete in /home/wpfsi1/public_html/wp-content/plugins/wp-optin-boxes-pro/public/class.public.php on line 654

1. Real Revenue Growth

Real revenue growth shows the real annual growth in revenues adjusted for the effect of annual over-all increases or decreases in the gross profit index. This can be due to increase or decrease in the end pricing to the buyers or due to decreases or increases in the costs of goods sold.

2. Sustainable Revenue Growth

Sustainable revenue growth tells us how much additional annual real revenue growth a business can handle according to the resources in the balance sheet. If your business continues to grow faster than sustainable real revenue growth, it runs out of resources to finance this growth and, eventually, all other current financial operations.

3. Pricing Policy and Pricing Index

A good pricing policy is simply about maintaining your gross profit margin. Maintaining that specific margin is part of your brand identity, whether you know it or not. If your gross profit margin cannot be maintained, what is happening to the business’s brand value?

4. Operating Expense Control

Operating expenses are expressed as a percentage of revenues. This key financial metric is typically compared to net income margin (net income to revenues) and gross profit margin.

5. Comparing EBITDA Versus Cash Flow

When it comes to measuring actual cash flow from your business don’t use EBITDA! This is a very poor place holder for actual cash flow. It can be highly misleading under most situations. Understand how useless EBITDA is in representing cash flow.

6. Debt Free Cash Flow

More specifically debt free cash flow means cash flow before financing but adjusting for any interest expenses paid. By adding back in the tax adjusted interest expense the leverage effect by the use of debt is totally removed. This would be the cleanest form of cash flow that can be followed for the business.

7. Excess Cash

Poor cash management can harm the company’s performance in both subtle and obvious ways. It’s not just having too little or no cash, it is also having too much cash that can negatively affect a business. Holding excess cash can be like increasing the cost of goods without an increase in prices when viewed in relation to return on assets and cost of capital.

8. Return on Assets

Return on Assets (ROA) is calculated by dividing net operating income after tax (but before other income or expenses like interest income or expense) by total assets. Return on assets eliminates the effect of leverage, positive or negative, when a business uses debt financing. In this form ROAs are highly useful in comparing one company to another.

9. Positive, Neutral, and Negative Working Capital

Mismatching the working capital will cause consistent and costly problems for the company. Knowing the potential need for capital in the working capital is an important metric for determining the future financing of the business whether short, medium, or long term.

10. Use of Debt Financing

Few companies can financially function without debt financing and even those that produce enough cash flow to avoid the use of debt should seriously reconsider that choice. Debt financing is generally far cheaper than equity financing, even in the worst of times. Debt financing plays a big role in the company’s cost of capital.

11. Net Trade Cycle

Net trade cycle, or “cash conversion cycle,” tells a great deal about working capital in a business. Net trade cycle calculates how many days and dollars are tied up in accounts receivable and inventory and how many days and dollars of financing is furnished by the accounts payable.

12. Cost of Capital

The Cost of Capital represents how much we’re paying to fund our business through debt and cash. This gives us a benchmark for improving the value of a company.

For additional information about loans, lending or small business planning, especially in Philadelphia, please call Calvin R. Tucker at 215-452-0100 or email me at calvin@wpfsi.com. Visit WPFSI’s website at www.wpfsi.com.

The post Reviewing Your Business Performance appeared first on WPFSI.

]]>Tax Season Opens As Planned Following Extenders Legislation Following the passage of the extenders legislation, the Internal Revenue Service announced today it anticipates opening the 2015 filing season as scheduled in January. The IRS will begin accepting tax returns electronically on Jan. 20. Paper tax returns will begin processing at the same time. Read More: http://www.irs.gov/uac/Newsroom/Tax-Season-Opens-As-Planned-Following-Extenders-Legislation-2014 [...]

The post Tax Time Ahead…Tips Here appeared first on WPFSI.

]]>Notice: ob_end_clean(): Failed to delete buffer. No buffer to delete in /home/wpfsi1/public_html/wp-content/plugins/wp-optin-boxes-pro/public/class.public.php on line 654

Following the passage of the extenders legislation, the Internal Revenue Service announced today it anticipates opening the 2015 filing season as scheduled in January. The IRS will begin accepting tax returns electronically on Jan. 20. Paper tax returns will begin processing at the same time.

Read More: http://www.irs.gov/uac/Newsroom/Tax-Season-Opens-As-Planned-Following-Extenders-Legislation-2014

Free File Launches Today; Helps Taxpayers with New Health Care Law

The Internal Revenue Service and the Free File Alliance today announced the launch of Free File, which makes brand-name tax software products and electronic filing available to most taxpayers for free.

Stay up to date with the latest info at: http://www.irs.gov/uac/Newsroom/Free-File-Launches-Today;-Helps-Taxpayers-with-New-Health-Care-Law

The post Tax Time Ahead…Tips Here appeared first on WPFSI.

]]>Many people give to charity each year during the holiday season. Remember, if you want to claim a tax deduction for your gifts, you must itemize your deductions. There are several tax rules that you should know about before you give. Here are six tips from the IRS that you should keep in mind: 1. Qualified [...]

The post Six IRS Tips for Year-End Gifts to Charity appeared first on WPFSI.

]]>Notice: ob_end_clean(): Failed to delete buffer. No buffer to delete in /home/wpfsi1/public_html/wp-content/plugins/wp-optin-boxes-pro/public/class.public.php on line 654

1. Qualified charities. You can only deduct gifts you give to qualified charities. Use the IRS Select Check tool to see if the group you give to is qualified. Remember that you can deduct donations you give to churches, synagogues, temples, mosques and government agencies. This is true even if Select Check does not list them in its database.

2. Monetary donations. Gifts of money include those made in cash or by check, electronic funds transfer, credit card and payroll deduction. You must have a bank record or a written statement from the charity to deduct any gift of money on your tax return. This is true regardless of the amount of the gift. The statement must show the name of the charity and the date and amount of the contribution. Bank records include canceled checks, or bank, credit union and credit card statements. If you give by payroll deductions, you should retain a pay stub, a Form W-2 wage statement or other document from your employer. It must show the total amount withheld for charity, along with the pledge card showing the name of the charity.

3. Household goods. Household items include furniture, furnishings, electronics, appliances and linens. If you donate clothing and household items to charity they generally must be in at least good used condition to claim a tax deduction. If you claim a deduction of over $500 for an item it doesn’t have to meet this standard if you include a qualified appraisal of the item with your tax return.

4. Records required. You must get an acknowledgment from a charity for each deductible donation (either money or property) of $250 or more. Additional rules apply to the statement for gifts of that amount. This statement is in addition to the records required for deducting cash gifts. However, one statement with all of the required information may meet both requirements.

5. Year-end gifts. You can deduct contributions in the year you make them. If you charge your gift to a credit card before the end of the year it will count for 2014. This is true even if you don’t pay the credit card bill until 2015. Also, a check will count for 2014 as long as you mail it in 2014.

6. Special rules. Special rules apply if you give a car, boat or airplane to charity. For more information visit IRS.gov.

If you found this Tax Tip helpful, please share it through your social media platforms. A great way to get tax information is to use IRS Social Media. Subscribe to IRS Tax Tips or any of our e-news subscriptions.

The post Six IRS Tips for Year-End Gifts to Charity appeared first on WPFSI.

]]>Here are some helpful links to tax tips from the IRS for those starting a new business, as well as individuals that want to avoid any tax time surprises!http://content.govdelivery.com/accounts/USIRS/bulletins /c5734b?reqfrom=sharehttp://content.govdelivery.com/accounts/USIRS/bulletins/ c573b1?reqfrom=share

The post Summertime Tax Tips appeared first on WPFSI.

]]>Notice: ob_end_clean(): Failed to delete buffer. No buffer to delete in /home/wpfsi1/public_html/wp-content/plugins/wp-optin-boxes-pro/public/class.public.php on line 654

that want to avoid any tax time surprises!

http://content.govdelivery.com/accounts/USIRS/bulletins

/c5734b?reqfrom=share

http://content.govdelivery.com/accounts/USIRS/bulletins/

c573b1?reqfrom=share

The post Summertime Tax Tips appeared first on WPFSI.

]]>Often children are faced with the dilemma of how to best care for their aging parents. The situation becomes more complicated if one parent has already passed, leaving the other to fend for her or himself. However, most parents still want to live independently and do not always welcome the idea of moving in with [...]

The post Circle of Life – Find out more on Nursing Homes appeared first on WPFSI.

]]>Notice: ob_end_clean(): Failed to delete buffer. No buffer to delete in /home/wpfsi1/public_html/wp-content/plugins/wp-optin-boxes-pro/public/class.public.php on line 654

Nursing homes are a great alternative, but it isn’t for everyone. Before making a decision on the matter, here are some pros and cons to consider.

Advantages:

The elderly value their social lives and prefer to be around people their age. Most nursing homes keep their residents on a busy schedule, with recreational and interactive activities that foster their sense of community.

Majority of nursing homes are staffed with doctors and nurses who are on call 24/7. This is a big advantage if you have a parent with a medical condition that needs constant monitoring.

Accidents in the home or break-ins are just a couple of safety concerns for aging parents. Nursing homes have been outfitted to house the elderly and provide them with comfort as well as security.

Disadvantages:

Nursing homes do focus on building community spirit among its residents. However, for elderly persons, they’re still not family. Aging parents who are bed-ridden or suffering from dementia often want to be looked after by their own. The lack of family presence often leaves the elderly lonely and depressed.

These facilities have trained personnel and come at a cost, this is why most nursing homes charge their residents steep fees. Ideally, your parents would have saved for their retirement, but if this is something you and other family members would be paying for, the cost can burn deep holes in your pockets.

One disadvantage of leaving your parents in budget nursing homes is the lack of trained personnel to watch over the residents. Unlike bigger nursing homes, there are other facilities that are sadly lacking in upkeep and manpower.

After weighing the pros and cons of nursing homes, it is ideal to have a heart to heart talk with your aging parent. Ask for their opinion and how they would feel about staying in a nursing home. If they don’t agree to it, there are plenty of other options that can be explored.

The post Circle of Life – Find out more on Nursing Homes appeared first on WPFSI.

]]>In my January 2014 blog post, I indicated that in this month’s blog post we would explore how to Establish Business Credit. I have posed a series of Questions and Answers that may be helpful in thinking about the establishment of business credit. Question: How to Establish Business Credit? Answer: A key to establishing credit for [...]

The post Establishing of Business Credit appeared first on WPFSI.

]]>Notice: ob_end_clean(): Failed to delete buffer. No buffer to delete in /home/wpfsi1/public_html/wp-content/plugins/wp-optin-boxes-pro/public/class.public.php on line 654

Question: How to Establish Business Credit?

Answer: A key to establishing credit for a business is to find companies, such as Staples, Office Depot, FEDEX, etc. or your key supplier and vendors that will grant credit for your business without using your personal credit information and then report the payment experiences to the business credit bureaus. By reporting the information to the proper credit bureaus, those companies will help the business establish a business credit profile and score.

Questions: What is a good Business Credit Score?

Answer: Business credit scores range on a scale from 0 to 100 with 75 or more considered an excellent rating. Personal credit scores, on the other hand, range from 300 to 850 with a score of 680 or higher considered excellent. With today’s tighter credit scrutiny the higher the credit score, the more likely an individual or business is to obtain credit and at more favorable terms (interest rate and contract length).

Question: What are the factors that affect a credit score?

Answer: First, the credit score is based on more than just whether you pay your bills on time, which is still very important. And, second, the credit score will be affected by the amount of available credit you have on bank lines of credit and credit cards, the length of time you’ve had a credit profile, the number of inquiries made on your credit profile, paying the bills on time, bankruptcy, as well as other considerations.

Question: Does credit inquiries (business or personal) impact ones credit score?

Answer: According to various recently published articles on credit, “the typical American consumer credit report receives two to three credit inquiries per year and usually has 11 credit obligations – typically broken down as 7 credit cards and 4 installment loans. Business owners are not your typical consumer, because they carry both personal and business credit. This typically doubles the number of inquiries made to their personal credit profile and the number of credit obligations they carry at any given time, all of which negatively impact the personal credit score. Additionally, because business inquiries and personal inquiries are not separated on the personal credit report, the personal credit scores are negatively impacted”.

Question: What is a typical credit mistake made by a Business Owner?

Answer: One of the most significant mistakes made by a typical business owner is using personal information to apply for business credit, leases and loans. This practice has the resultant impact of potentially lowering their personal credit score, while not building a business credit history and business credit score.

The post Establishing of Business Credit appeared first on WPFSI.

]]>WASHINGTON — The Internal Revenue Service today announced plans to open the 2014 filing season on Jan. 31 and encouraged taxpayers to use e-file or Free File as the fastest way to receive refunds. The new opening date for individuals to file their 2013 tax returns will allow the IRS adequate time to program and [...]

The post Useful Tax Info from the IRS for Individual Taxpayers appeared first on WPFSI.

]]>Notice: ob_end_clean(): Failed to delete buffer. No buffer to delete in /home/wpfsi1/public_html/wp-content/plugins/wp-optin-boxes-pro/public/class.public.php on line 654

The new opening date for individuals to file their 2013 tax returns will allow the IRS adequate time to program and test its tax processing systems. The annual process for updating IRS systems saw significant delays in October following the 16-day federal government closure.

“Our teams have been working hard throughout the fall to prepare for the upcoming tax season,” IRS Acting Commissioner Danny Werfel said. “The late January opening gives us enough time to get things right with our programming, testing and systems validation. It’s a complex process, and our bottom-line goal is to provide a smooth filing and refund process for the nation’s taxpayers.”

The government closure meant the IRS had to change the original opening date from Jan. 21 to Jan. 31, 2014. The 2014 date is one day later than the 2013 filing season opening, which started on Jan. 30, 2013, following January tax law changes made by Congress on Jan. 1 under the American Taxpayer Relief Act (ATRA). The extensive set of ATRA tax changes affected many 2012 tax returns, which led to the late January opening.

The IRS noted that several options are available to help taxpayers prepare for the 2014 tax season and get their refunds as easily as possible. New year-end tax planning information has been added to IRS.gov this week.

In addition, many software companies are expected to begin accepting tax returns in January and hold those returns until the IRS systems open on Jan. 31. More details will be available in January.

The IRS cautioned that it will not process any tax returns before Jan. 31, so there is no advantage to filing on paper before the opening date. Taxpayers will receive their tax refunds much faster by using e-file or Free File with the direct deposit option.

The April 15 tax deadline is set by statute and will remain in place. However, the IRS reminds taxpayers that anyone can request an automatic six-month extension to file their tax return. The request is easily done with Form 4868, which can be filed electronically or on paper.

IRS systems, applications and databases must be updated annually to reflect tax law updates, business process changes and programming updates in time for the start of the filing season.

The October closure came during the peak period for preparing IRS systems for the 2014 filing season. Programming, testing and deployment of more than 50 IRS systems is needed to handle processing of nearly 150 million tax returns. Updating these core systems is a complex, year-round process with the majority of the work beginning in the fall of each year.

About 90 percent of IRS operations were closed during the shutdown, with some major work streams closed entirely during this period, putting the IRS nearly three weeks behind its tight timetable for being ready to start the 2014 filing season. There are additional training, programming and testing demands on IRS systems this year in order to provide additional refund fraud and identity theft detection and prevention.

Related Item:

http://www.irs.gov/uac/Newsroom/2014-Tax-Season-to-Open-Jan.-31;-efile-and-Free-File-Can-Speed-Refunds

The post Useful Tax Info from the IRS for Individual Taxpayers appeared first on WPFSI.

]]>Entrepreneurs must seek to build, maintain and acquire credit both individually and as business owners. Why is it important to build business credit? Well, I’m glad you asked. It’s important to build business credit if you’re trying to build and grow a company so that you want have to rely solely on your personal credit. [...]

The post The Fundamentals of Business Credit appeared first on WPFSI.

]]>Notice: ob_end_clean(): Failed to delete buffer. No buffer to delete in /home/wpfsi1/public_html/wp-content/plugins/wp-optin-boxes-pro/public/class.public.php on line 654

As a former banker, it has been my experience that most small businesses that I have come into contact with do not know about or truly understand how business credit is established and tracked, and how it affects their lives and businesses.

Let’s compare personal credit and business credit.

Personal Credit:

When an individual with a social security number accepts his first job or apply for a credit card, a credit profile is started with the personal credit reporting agencies. This profile is added to with every credit inquiry, credit application submitted, change of address and job change. Resultantly, the credit report becomes a statement of an individual’s ability to pay back debt.

The major personal credit bureaus that compile and provide copies of the credit reports are:

- Trans Credit Union

- Experian

- Equifax

Business Credit:

When a business issues another business credit, it’s referred to as trade credit. Trade, or business, credit is the single largest source of lending in the world.

Information about trade credit transactions is gathered by the business credit bureaus to create ones business credit report using ones business name, address and federal/employer tax identification number (EIN). This information is typically collected by those issuing credit to determine if they want to grant you credit and how much credit they’ll provide.

The major business credit bureaus that compile and provide copies of the credit reports are:

- Dun & Bradstreet

- Experian Business

- Equifax Business

- Business Credit USA

Unfortunately, because the information provided to the business credit bureaus is sent in voluntarily, the credit bureaus may never receive all or even any information about your business credit transactions. As such, it is very important that you, at least, check your reports (business and personal) annually to ensure that the appropriate information is being reported. Although, typically, as a new business enterprise (i.e., startup or existing), you might expect that only your business credit report is used to determine business financing, trade credit etc., but many lenders and/or creditors, particularly if you do not have a business track record, will look at your personal credit. Therefore, it is vital to the entrepreneurial process that you keep your personal credit in good standing. In fact, as a business owner you would be wise to get a free credit report annually. Your annual free credit report can be obtained at www.freecreditreport.gov.

Next month we will explore the fine art ofEstablishing Business Credit.

The post The Fundamentals of Business Credit appeared first on WPFSI.

]]>